As a general rule, we recommend that you do not deliver a notice of a right of rescission (ROR) when the customer (or other consumer who has an ownership interest in the property securing the loan) is not entitled to Regulation Z’s right of rescission.

The ROR under Regulation Z does not apply to a refinancing by the original creditor for a closed-end loan secured by the borrower’s principal dwelling when no new money is advanced (i.e., when the amount refinanced does not exceed the original loan’s unpaid principal balance). 12 CFR 1026.23(f)(2). Consequently, not all of your refinancing customers will be entitled to the right to rescind a transaction under Regulation Z.

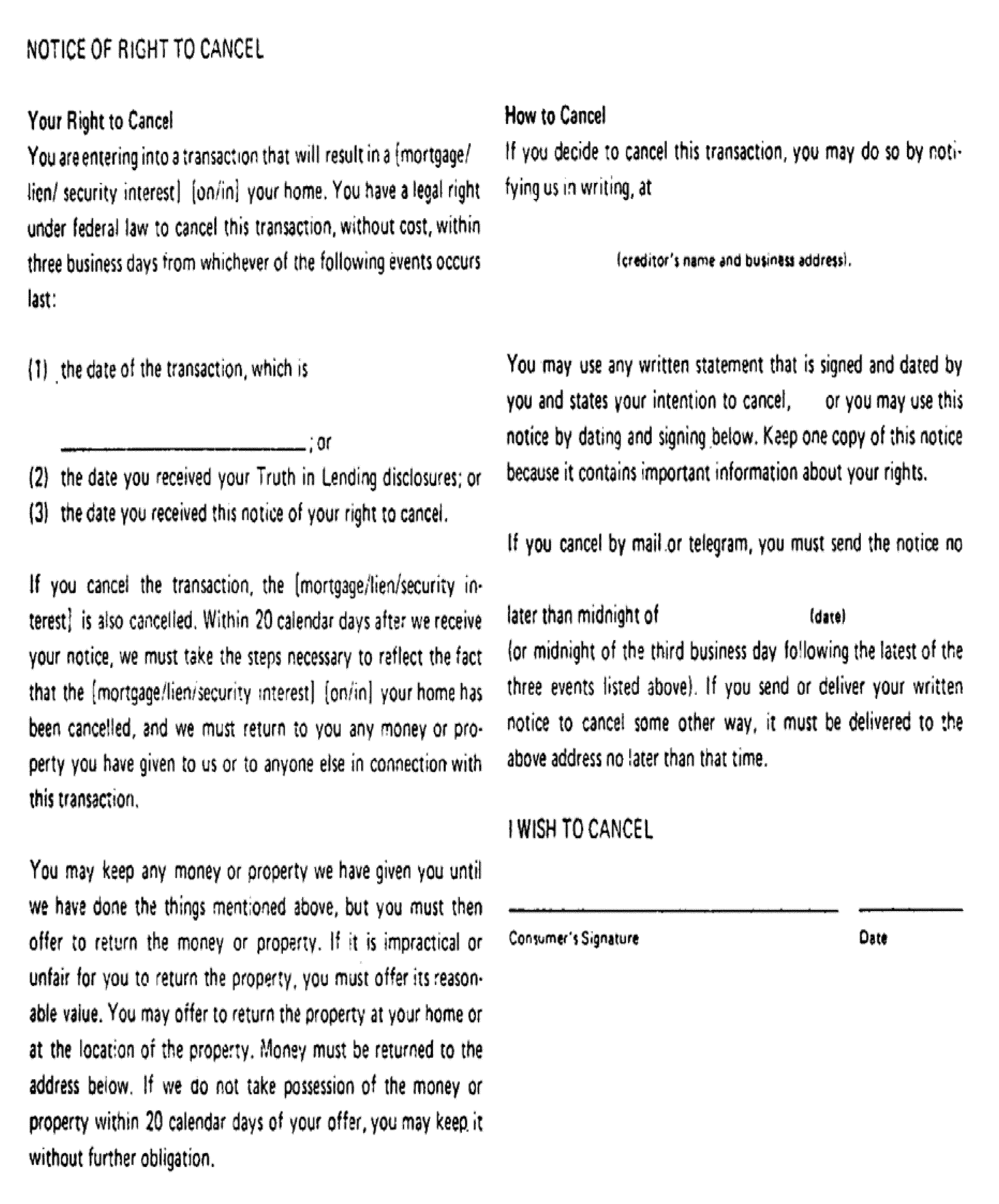

If you provide an ROR notice to customers who are not entitled to this right, the language of the notice may confuse those customers. Specifically, as the model ROR notice in Regulation Z states: “You have a legal right under federal law to cancel this transaction.” This clearly is an inaccurate statement for transactions that fall into the refinancing exception described above. In addition, if you are using the regulation’s model form for refinancings where no new money is advanced, the ROR notice will inaccurately state that the customer is “entering into a new transaction to increase the amount of credit previously provided to you.” See Appendix H to Part 1026, Forms H-8 and H-9.

{kind=link}

By providing these notices in refinancings when no new money is advanced, you may be contractually granting an ROR to customers who would not otherwise be entitled to rescind their transactions, or, at a minimum, you could be subject to charges of having provided false and misleading statements. While we are not aware of any court decisions that address these issues, providing such notices could give rise to costly litigation over them.

We should note that your bank also could elect to contractually provide RORs to customers even when not required to do so under Regulation Z. However, if you elect to provide a contractual ROR, you would need to revise the Regulation Z notices, which still would be inaccurate and confusing in such situations, as noted above.

In sum, assuming that you want to avoid extending a contractual right of rescission to your consumer customers who are not eligible for that right under Regulation Z, we recommend that you provide the ROR notices only to consumers who are eligible for the right under Regulation Z.